.svg)

.svg)

.svg)

.svg)

.svg)

On the surface, spending still looks steady. But once you look closer, the pattern underneath is a bit harder to read. You can see that people are buying, but they’re pausing longer before they commit. And while price pressure is everywhere, values still shape where money actually goes.

So the tension is not whether demand exists, but how decisions now get made. Also, signals that once felt reliable no longer line up cleanly. That gap is exactly what makes global consumer spending trends harder to act on with confidence.

So, this article breaks down what’s changing and why those shifts feel contradictory. It also shows how you can respond with clearer judgment, without guessing.

Let's get started!

TL;DR: Global Consumer Spending Trends at a Glance

- Spending continues, but decisions take longer and feel heavier.

- Value-hunting replaces loyalty, with baskets split across stores.

- Convenience matters more than patience across delivery, checkout, and returns.

- Cashless payments shape conversion and not just checkout speed.

- BNPL becomes part of everyday planning, especially for younger buyers.

- Subscriptions grow, but retention depends on control and flexibility.

- Experiences win budget share over physical goods.

- Health and wellness spend feels preventative rather than indulgent.

- Sustainability shifts from optional to expected.

- Digital channels influence choice, but trust decides the final click.

What Consumer Spending Trends Really Mean Today

Consumer spending trends reflect shifts in when decisions happen, how tradeoffs are made, and where confidence breaks or holds. In practice, the signal comes from consumer behavior changing under pressure, where the same shopper spends, hesitates, and switches more often.

And because pressure exposes habits, small changes now carry outsized impact at scale. That’s why reading global consumer spending trends as forecasts leads teams astray. They show behavior already in motion rather than what might happen later.

So context matters. When money is tight unevenly, patterns fragment across categories, channels, and cohorts. These shifts are shaped by interest rates, uneven labor market conditions, and fragile consumer confidence.

That’s why topline data can look stable while decisions feel slower and less predictable. In fact, Deloitte expects real consumer spending growth to slow to 1.6% in 2026, down from an anticipated 2.6% in 2025. This explains why mixed signals persist even as spend continues.

For a quick real-world take on why spending data can look mixed, watch this short video from Simeon Siegel:

Now, the patterns start to matter.

What Are the Top 10 Consumer Trends Right Now?

People haven’t stopped buying. They’ve changed how they buy. The path from interest to purchase is longer and more influenced by trust, proof, and convenience than it was even a few years ago. The trends below capture the changes that are already affecting demand, expectations, and brand performance.

1. “Value-Hunting” Becomes the Default

Value-hunting is not really reduced buying, it’s active comparison. Today, you can notice baskets split across stores, price checks before each add-to-cart, and deal-chasing item by item across online shopping and physical aisles.

This behavior scales because pressure exposes habits. As consumer attitudes tighten, shoppers work harder to keep personal spending within limits without cutting lifestyle outright.

That context matters because ELMA finds that around 60% of weekly shoppers choose retailers mainly on price differences, and 76% regularly visit two or more stores. This is evidence that consumer transactions are spreading rather than shrinking across categories and retail sales environments.

So the risk is misreading this as churn. What actually breaks loyalty is friction. So, to respond, make comparisons simple where decisions happen.

This means clear unit pricing, bundles that show savings without math, and private labels positioned as practical swaps rather than compromises. That approach supports consumption concentration without racing to the bottom on price.

Pro tip: Value perception usually comes from clarity and not from lower prices. For instance, inBeat Agency used creator-led UGC ads for Hopper to simplify decision-making. This helped the company reduce acquisition costs while scaling installs across markets.

Here's an example of our work:

2. The “Uncommitted Customer” Keeps Growing

Uncommitted customers often look loyal in reports, but behave far more fluidly in real life. Membership numbers go up, while actual buying patterns spread across more brands, more channels, and more formats as shoppers try to protect disposable income.

The gap grows because loyalty now competes directly with convenience, price, timing, and availability, not just brand preference. Purchases happen when conditions line up, not simply because points exist.

That explains why the average U.S. consumer belongs to about 16.7 loyalty programs but actively engages with only 6-7. It's clear that membership signals intent and not commitment. So the mistake is adding more perks without reasons to return.

Instead, you should focus on a growth strategy built around cadence. Create always-on deals tied to everyday needs, fast rotations that reward checking back, and simple perks that remove friction. When returns feel easy and worthwhile, engagement follows without forcing commitment.

3. Convenience Wins (and Patience Drops)

Convenience is now one of the strongest forces behind where money actually goes, even when budgets are under pressure. “Bring it to me” behavior continues across online retail, grocery delivery, and food services, because time and mental effort feel just as limited as cash.

As routines get denser, tolerance gets thinner. Delays, complicated returns, or vague delivery windows break momentum fast. That pressure is a big reason e-grocery and on-demand categories keep growing. According to GroceryDive, penetration now reaches about 61% of U.S. households, or roughly 81 million people. This shows how deeply convenience has moved into US personal spending habits.

So the risk is assuming speed alone solves it. What actually matters is reliability across the full journey. Improving delivery windows, pickup flexibility, and return clarity reduces friction where service spending concentrates.

Then communicate those changes clearly, because confidence typically comes from knowing what will happen next rather than from faster promises.

Pro tip: Wondering why fast, convenient experiences stop working when creative stays the same? See how creative fatigue shows up in performance signals in this creative fatigue guide.

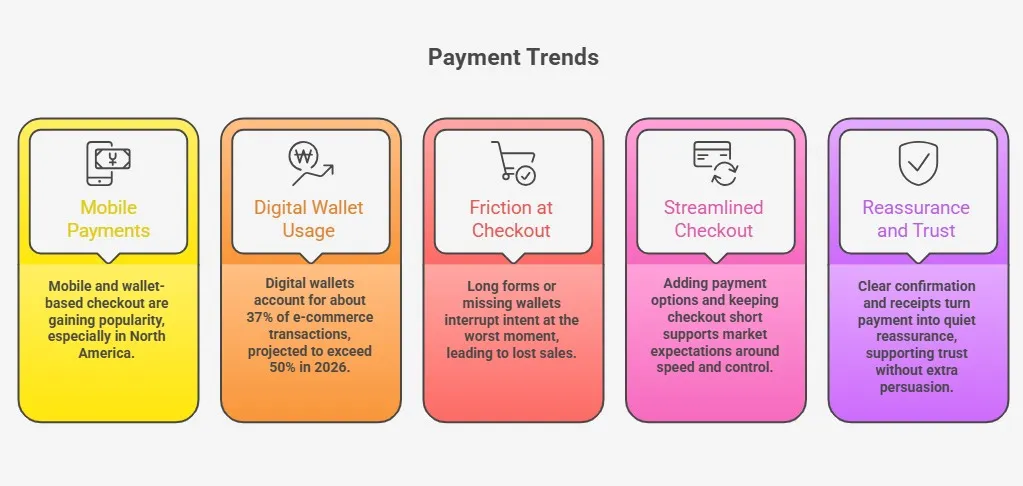

4. Cashless Keeps Rising, and Payments Become Part of the Product

Payments are no longer just the end of the journey; they influence whether a purchase occurs at all. Mobile and wallet-based checkout have gained ground as phone-first buying becomes routine, especially in North America.

That shift changes expectations since any extra step now feels like hesitation built into the product itself. This pattern shows up clearly in consumer expenditures, where digital wallets already account for about 37% of e-commerce transactions, with projections pointing past 50% in 2026.

Friction at checkout carries a real cost. Long forms or missing wallets interrupt intent at the worst moment.

So, adding widely used payment options and keeping checkout short supports market expectations around speed and control. When paired with clear confirmation and receipts, this turns payment from a barrier into quiet reassurance, which supports trust without extra persuasion.

5. Buy-Now-Pay-Later Expands Past “Nice to Have”

Buy-now-pay-later now plays a structural role in how purchases get approved. We can see it used less as a last resort and more as a planning tool, especially as spend spreads across more categories.

That shift tracks closely with younger buyers managing limited buffers in their bank accounts while trying to maintain everyday choices. This is most visible among Gen Z, where BNPL feels normal rather than exceptional.

In fact, adoption data clearly show the scale. About 59% of Gen Z and 58% of Millennials use BNPL services. This explains why deferred payment has moved into routine checkout behavior.

So the risk is hiding BNPL or treating it like a promotion. What actually works is clarity. You can place options where decisions happen, explain costs in plain terms, and avoid surprises later. When terms are clear, BNPL supports intent without increasing regret or drop-off.

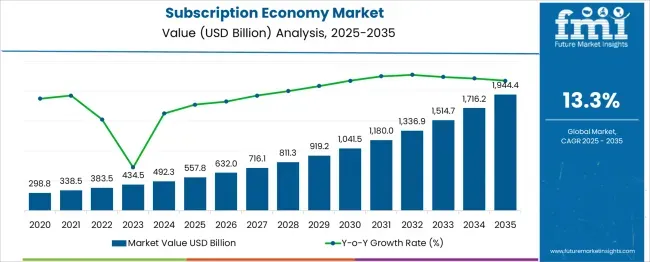

6. Subscriptions Keep Growing, But Buyers Expect Real Value

Subscriptions keep expanding because predictability can feel safer than one-off decisions. This happens across media, software, and even physical goods, where access matters more than ownership. When pressure builds, predictable billing helps manage personal consumption expenditures without the need for constant re-evaluation.

That dynamic explains why subscription models continue to scale. Consumer expenditure data from Future Market Insights shows the global subscription economy projected to grow from about $557.8 billion in 2025 to nearly $1,944.4 billion by 2035.

But growth hides tension. Buyers now audit value more frequently, especially as price increases ripple through the Consumer Price Index. So retention depends less on perks and more on control.

Flexible tiers, simple bundles, and easy canceling reduce friction and rebuild trust. When exit feels safe, commitment lasts longer without forcing loyalty that breaks under scrutiny.

Pro tip: Want to know what actually keeps buyers subscribed after the first few months? Our lifecycle maturity guide breaks down how brands build long-term value without relying on constant discount codes.

7. Experiences Stay a Top Spend Category

Experiences continue to hold a strong share of consumer spending because they’re harder to postpone than physical purchases. People invest in moments that can be lived, shared, and remembered. Even when other categories face tighter scrutiny, trips, getaways, and vacation plans keep moving forward.

That pattern can also be seen across regions. For example, in Europe, about 32% of consumers spent more than €1,000 on travel and tourism-related experiences in 2025.

But the behavior goes deeper. Social validation and milestone moments carry weight, especially across specific age groups. That’s why, in the U.S., around 84% of Millennials report spending the same or more on travel in 2025 than in 2024.

So the opportunity is not selling more products, but anchoring them to moments. Events, community access, and shareable add-ons help connect spend to meaning. This needs to be guided by sharper demographic insights rather than broad assumptions.

8. Health and Wellness Spend Rises (Food, Supplements, Routines)

Health and wellness spending grows because it feels preventative rather than indulgent. There's more money flowing into better-for-you food, supplements, and daily routines that promise stability.

When long-term health feels uncertain, these purchases look like control rather than cost. That’s why willingness to pay stays high. About 55% of consumers say they are open to spending more than $100 per month on nutrition, self-care, and physical or mental wellness products.

The tension is trust. Claims matter less than proof, especially in health care-adjacent categories where scrutiny runs high. So, clear benefits, simple labels, and consistent messaging can help you reduce hesitation at the shelf or screen.

When paired with careful use of digital marketing to reinforce credibility, wellness products move from impulse to habit. Once routines stick, spending follows without repeated persuasion.

9. Sustainability Shifts From “Nice” to “Expected”

Sustainability now affects whether a purchase feels acceptable rather than just appealing. You see buyers ask how products are made, where materials come from, and what happens after use. That scrutiny is present even during holiday shopping, when tradeoffs usually loosen.

As transparency becomes part of decision-making, pricing tolerance shifts as well. In fact, PwC found that many consumers are willing to pay about 9.7% more for sustainably produced or sourced goods, even when cost pressure stays high.

Here's what a leader from PwC had to say about this:

“Consumers are increasingly feeling the squeeze of inflation and rising prices in essential goods such as groceries, however in that context, they are prioritising products that are sustainably produced and sourced. Even as consumers look to cheaper, generic options for essentials, they nevertheless cite a willingness to pay 9.7% more for sustainability. In the year ahead, companies must achieve a delicate balance between consumer affordability and environmental impact if they are to source and retain consumers. They will also need to bolster their digital engagement and service-delivery, particularly as more consumers purchase products directly through social media.” - Sabine Durand-Hayes, Global Consumer Markets Leader

From this, we can learn that the risk is treating sustainability as a badge instead of a system. Claims without follow-through raise doubt.

What works better is visible action. This includes repair options, recycling paths, trade-ins, and clear sourcing details that hold up under review. When these choices are built into merchandising models, sustainability stops feeling like a premium add-on and starts feeling expected.

10. Digital Influences Purchases, But Trust Stays Tricky

Digital channels help buyers make decisions, even when trust feels fragile. Buyers research, compare, and decide, even before any direct brand contact. And while friends and family still matter, online signals increasingly frame the shortlist.

According to McKinsey, 32% of consumers now use social media for product research, up from 27% in 2023. This explains why digital touchpoints matter even outside peak moments like Black Friday.

But reach does not equal belief. Inconsistent messages or shallow creator use break confidence fast. So, what holds is proof. Reviews, creator credibility, and UGC content help close the gap when claims feel abstract.

You should keep messages aligned across channels, support sharing without friction, and treat digital presence as evidence. When trust builds gradually, conversion follows without pressure.

Pro tip: Brands that rely on real customer content see this play out in practice. For example, inBeat Agency helped BlueHouse Salmon scale trust through influencer reviews and everyday UGC. This helped them drive 1900% follower growth over a 12-month period without relying on polished brand claims.

Here's an example of our work:

Why Consumers Feel Cautious Even When Spending Continues

Consumers feel cautious even while spending continues because decision confidence has weakened faster than purchasing power.

On the emotional side, uncertainty is now present between intent and action. We can see this in longer consideration windows, repeated checks, and a need to feel “right” about timing before committing. Spending is still there, but it carries more mental weight than before.

At the same time, financial confidence is fragile. Many people are unsure whether they are making smart money choices, even when their income allows them to buy.

Only 47% of Americans say they feel confident in their ability to make good financial decisions. So every purchase carries a second question. It’s not “can this be afforded,” but “is this the right call?”

This creates a confidence gap. Behavior moves forward, but belief lags behind. Brands usually misread that gap as lost demand and react by cutting prices or pulling back. In reality, the issue is trust in judgment rather than willingness to spend.

Common Brand Mistakes When Reacting to Global Consumer Spending Trends

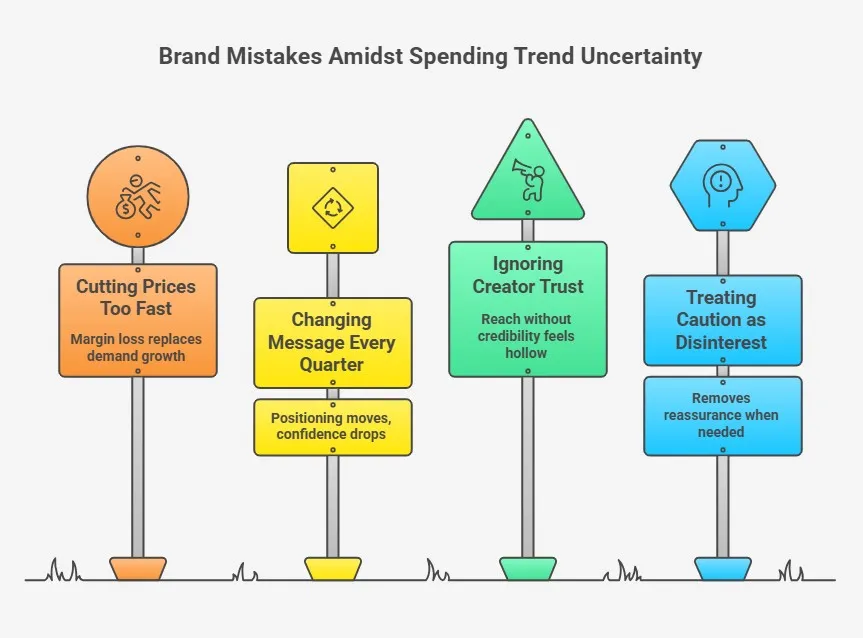

When signals are mixed, reaction usually replaces judgment. And under pressure, brands default to moves that feel safe but actually weaken their position. Here are the most common mistakes that show up when spending behavior gets harder to read:

- Cutting prices too fast: Lowering prices early trains buyers to wait and shifts focus away from value. Over time, margin loss replaces demand growth, and recovery becomes harder than expected.

- Changing message every quarter: Frequent narrative shifts create doubt. When positioning keeps moving, confidence drops, and buyers delay decisions, even if the offer stays strong.

- Ignoring creator trust: Reach without credibility feels hollow. When creator choices prioritize scale over fit, attention rises, but belief does not follow.

- Treating caution as disinterest: Hesitation typically signals evaluation rather than rejection. Pulling back too soon removes reassurance right when it is needed most.

What Smart Brands Do Differently

Smart brands respond by slowing decisions down just enough to learn before committing. Instead of scaling ideas on instinct, testing comes first, so signals get validated in the market before budgets move. And that discipline matters, because small shifts in behavior now create large effects once spending scales.

At the same time, trust becomes the real lever. Reach alone no longer carries weight when buyers hesitate. Instead, consistency, credibility, and repetition build belief over time, especially when decisions feel risky. So investment shifts from exposure to reassurance.

Then the content takes on a new role. It stops acting as decoration and starts working as proof. This includes clear demonstrations, real customer experiences, and consistent messages that reduce doubt at the moment of choice.

Together, these moves replace reactive tactics with measured learning. When judgment leads, and testing supports it, growth stays steady even as behavior stays hard to read.

Pro tip: This approach shows up clearly in performance-led creator programs. In one example, inBeat Agency tested and scaled micro-influencer content for GreenPark. This resulted in a 6x increase in daily installs while cutting acquisition costs.

Here's what we did:

How inBeat Agency Helps Brands Adapt to Consumer Spending Shifts

When spending behavior sends mixed signals, inBeat Agency helps you replace guesswork with evidence. Our team focuses on creator-led, data-backed content that tests how people actually decide before budgets scale.

And that approach shows up clearly in practice. For Dockers, inBeat’s creator content ran for 11 months with 82 creators. This generated 15.8M views and 167K content interactions, and the paid push delivered 596K total brand lift ad recalls.

Apart from that, we noticed a jump from 140K to 286K in one month as the frequency increased to 2.35. That’s proof repeated exposure can still build familiarity, even when loyalty fragments.

At the same time, performance-driven creator testing helps separate attention from belief. Instead of assuming reach equals impact, content gets tested for recall, message clarity, and confidence signals first, then expanded only when results hold.

This way, decisions are grounded in real behavior. The focus on content as evidence helps inBeat to turn creator work into buying confidence, which is exactly where hesitation tends to slow growth today.

Here's an example of our work with Dockers:

Ready to Turn Spending Signals Into Better Decisions?

Consumer spending hasn’t vanished, but it has matured. What looks like hesitation is usually careful judgment playing out in real time. And when brands pause to listen instead of reacting fast, patterns become clearer and risk drops. So spending trends stop feeling like warnings and start acting like signals.

The brands that win read those signals calmly, test before committing, and stay consistent, while others overcorrect. That discipline turns uncertainty into direction and effort into learning.

For support that turns real behavior into confident decisions, reach out to inBeat Agency and see how measured testing can guide your next move.